What is the proposed change?

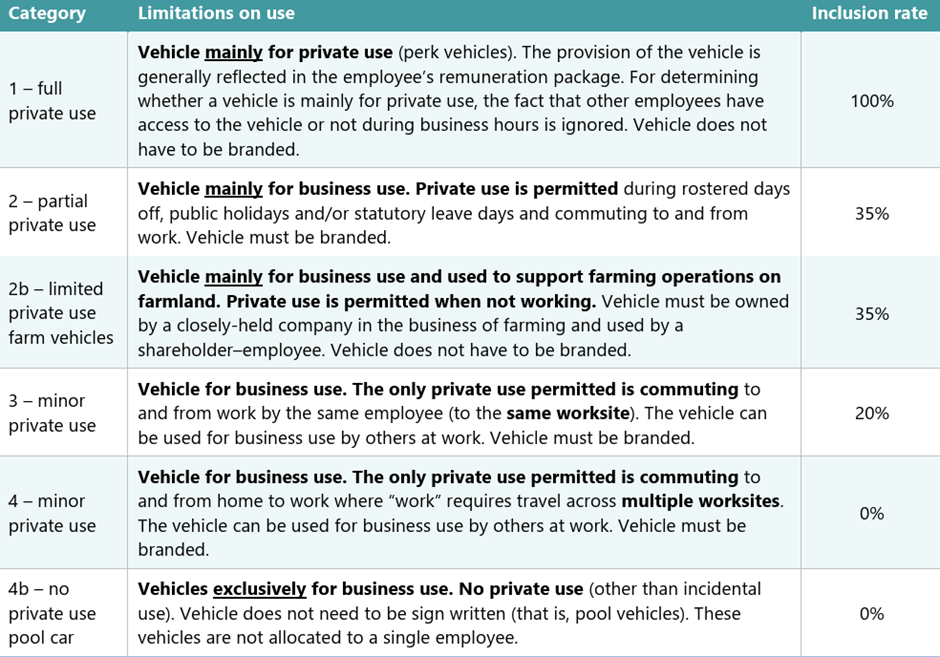

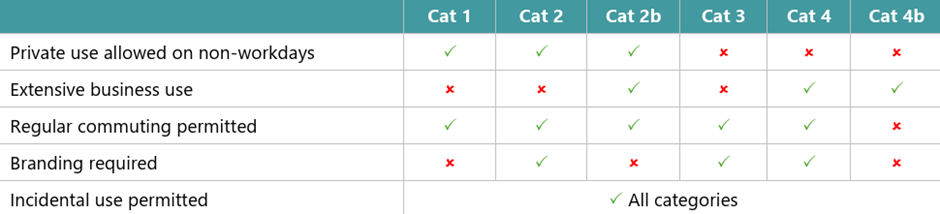

The main proposal would simplify the way fringe benefit tax (FBT) applies to motor vehicles by implementing a “category approach”. FBT is currently based on employers counting the days a vehicle is available for an employee’s private use. This proposal would remove counting days and instead require employers to choose a category (based on the private use of the vehicle) and use that rate when calculating their FBT liability.

An employer would select a category upfront when providing a vehicle to an employee and would only need to revisit this if the expected private use changes materially. These proposed categories are explained in the table below.

Categories of vehicle use for FBT purposes:

Incidental use (use that is infrequent or ad hoc) would not impact the classification of the vehicle or be subject to FBT. The purpose of this rule would be to remove those situations when there is private use of a work vehicle, but it is not remunerative or a substitute for remuneration. For example, an employee using a work van one weekend to move. What about work-related vehicles? The proposal would remove existing exemptions (such as the work-related vehicle exemption) because these should be captured within the categories. These should better reflect the range of vehicle use available for employees. For certain emergency vehicles, there would be a new exemption that would totally exempt these vehicles from the FBT regime.

Source: IRD – https://www.ird.govt.nz/employing-staff/deductions-from-other-payments/fringe-benefit-tax/types/motor-vehicles/about

Disclaimer

Unfortunately, with details changing all the time and at such speed, we need to add that the above content is correct at the time of writing as far as the author is aware and is very much subject to change. We have, to the best of our ability, acknowledged any shared content. All related links provided to the corresponding websites are subject to change as they are live links.